How much is Bitcoin worth? This literally is the Million-Dollar Question. This article has a look at a novel approach using a combination of brand value and cash flows into Bitcoin.

Disclaimer: This is not investment advice! I’m not a financial advisor but simply want to share a new methodology to value Bitcoin.

Table of Contents

Valuation Idea

We will obtain a dollar valuation for 1 BTC by using the following approach:

- Bitcoin is among the world’s most well-known brands with significant exposure in books, videos, podcasts, blog posts, research papers, personal conversations and all other means of communication.

- First, we will approximate how much a corporation would have to spend to gain a similar type of exposure from a brand-marketing point of view.

- Second, a certain fraction of people who are exposed to the Bitcoin brand in a given point in time will decide to purchase the BTC token. Thus, Bitcoin’s brand marketing results in capital flows into the BTC ecosystem.

- Third, we take the following perspective: the capital that flows into the Bitcoin “corporation” is a revenue stream of the Bitcon corporation, similar to the cash flows of a corporation such as Google, Facebook, or Amazon. These cash flows directly benefit all holders of Bitcoin (BTC) because it leads to an appreciation of the value of their coins. If $21,000,000 flows into Bitcoin, the fair value of 1 BTC has increased by $1 because 1 BTC is and will ever be 1/21 millionth of all available BTC.

- Forth, all this revenue is profit for the Bitcoin holders as the Bitcoin organism doesn’t pay for its brand exposure but gets it for free. All other costs such as mining are paid for separately by means of transaction revenue. As this has no effect on this valuation, we ignore these revenues in this valuation model.

- Fifth, having obtained the annual profit of the Bitcoin network, we can calculate the annual profit (or cash flow) that goes into a single BTC. We can use this to employ traditional valuation tools for assets such as discounted cash flow analysis or simple P/E based valuation.

Let’s get started!

Bitcoin Brand Value

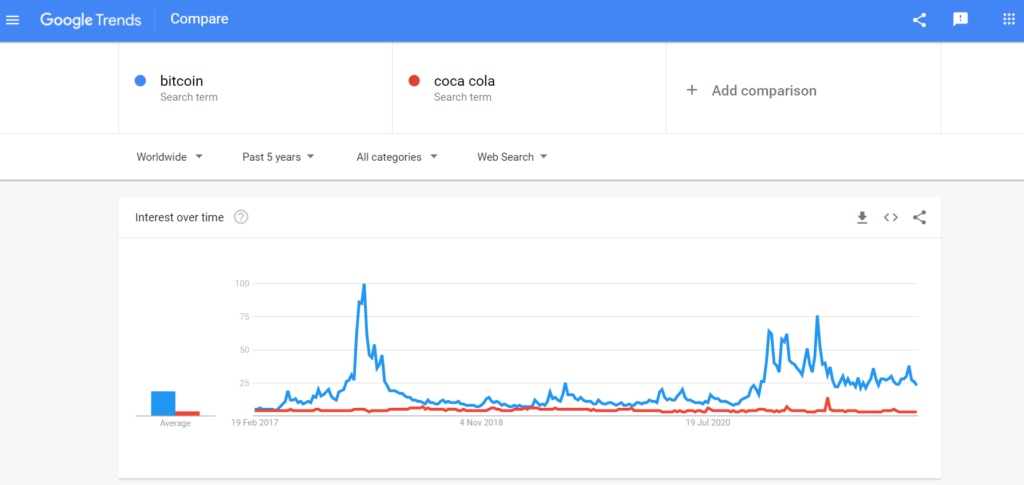

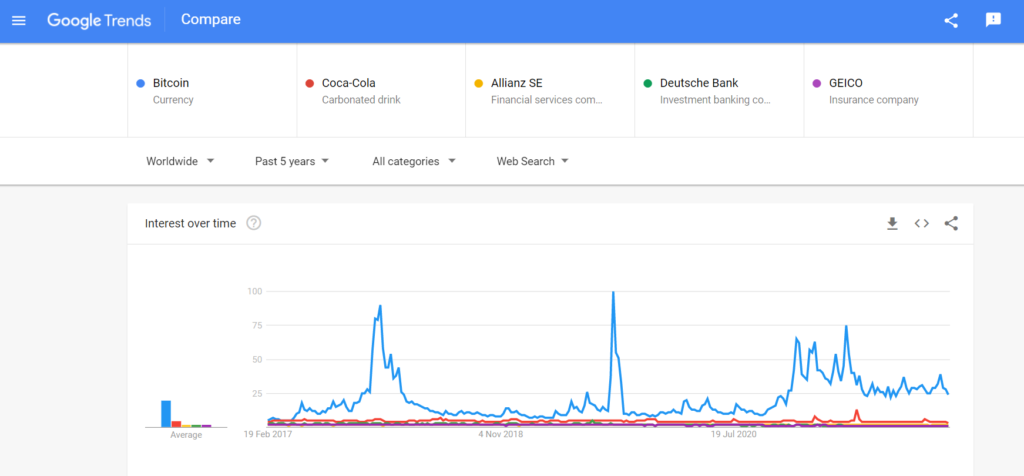

Let’s compare Bitcoin against different brands by using Google search volume to estimate the search volume:

Here are a couple of more comparisons to get a feeling on how much search volume there is:

If we summarize these results, we obtain a rough estimate of the strength of the Bitcoin brand:

| Bitcoin | Coca Cola | Allianz | Deutsche Bank | GEICO |

|---|---|---|---|---|

| 20 | 5 | 2 | 2 | 2 |

Bitcoin has 4x the direct brand queries of Coca-Cola and 10x more brand queries than Allianz, Deutsche Bank, and GEICO. I chose the latter three because, like Bitcoin, these are brands in the financial sector.

Here’s what these brands spent on marketing in the year 2020:

- Coca-Cola spends $4B per year on advertisments (source). Note that these are direct advertisement costs and it doesn’t include the marketing costs from the large network of bottlers and Coca-Cola resellers.

- Allianz spends $29B per year on sales and marketing (source). Much of this is commissions on insurance agents—Bitcoin doesn’t need to pay its insurance agents but gets the same value!

- Deutsche Bank spends $19B per year on sales and marketing (source).

- GEICO spends more than $1.6B per year on advertising alone (source).

According to some studies (e.g., here), more than 89% of Americans know about Bitcoin. Billions of people worldwide know the Bitcoin brand, so it is far more well-known than GEICO or Allianz.

Clearly, for a company to obtain this amount of exposure, it will cost many billions of USD on a recurring basis. More specifically, there are at least two ways to estimate the annual “marketing value” of the Bitcoin brand:

- Comparative: Bitcoin has 4x more search volume than Coca Cola that spends $4B. So, a lower bound of Bitcoin’s marketing benefit would be $16B. GEICO spends north of $1.6B on ads to obtain one tenth of the exposure. This would also place the value (or cost of duplicating) Bitcoin marketing efforts on $16B.

- Performance Marketing (Cost-per-click): Assuming 80% of people have heard of Bitcoin. Further assuming that they are exposed to Bitcoin at least once per month on average through a personal interaction, by watching a YouTube video about Bitcoin, seeing it mentioned in a movie, or by reading an article online — or any other means of communication. With 7.7B people in the world, Bitcoin gets 7.7B x 80% x 12 (months) = 73B impressions per year. What would be the cost of acquiring that many impressions? Assuming a moderate price of $60 per 1000 impressions, this equates to a marketing benefit of 73B * $60 / 1000 = $4B. Note that this really is a super pessimistic estimation of the marketing benefit because reading a Bitcoin article or talking with a friend about Bitcoin is a much more high quality interaction than, say, skimming over a third-party ad. So, in reality, the marketing benefit could easily be 10x higher.

So, assuming the annual marketing benefit of Bitcoin is $10B which is well within the [$4B, $16B] pessimistic range. In other words, if you wanted to replicate brand exposure similar to the Bitcoin brand, you’d have to spend at least $10B per year—probably much more just for marketing.

In performance marketing, you lay out ad-spend today to get more back tomorrow. Assuming that each $1 marketing equivalent value spent by the Bitcoin corporation results in the “conversion event” of $2 inflow into the Bitcoin corporation (“return on ad spent” is 2x-5x). This is typical for many companies using performance advertisments such as Fiverr and Upwork (see their annual filings here).

Consequently, a conservative estimation for BTC’s net income is $20B, money that directly flows into the Bitcoin corporation every year to purchase the BTC token from the existing token holders.

Here’s a table of different scenarios for the Bitcoin marketing value, ROI of marketing value, and resulting net income in the Bitcoin network.

| Bitcoin Marketing Value | ROI | Bitcoin Net Income |

|---|---|---|

| $1B | 0.1x | $0.1B |

| $10B | 1x | $10B |

| $10B | 2x | $20B |

| $10B | 10x | $100B |

| $20B | 15x | $300B |

You can see that the net income numbers, i.e., the cash flows into the Bitcoin “corporation”, are between $0.1B and $300B with these assumptions. I left the range wide on purpose to reduce the number of my personal assumptions going into this model. My personal estimation would be more towards the higher end of this range. This is how much the Bitcoin corporation earns for its BTC tokenholders, every year.

Note that you need to use your own numbers for this—the purpose of this article is just to give you a way to value Bitcoin based on performance marketing equivalence and obtain a cash flow for further valuations.

You can now use these net income numbers to obtain your own valuation of the Bitcoin corporation. For example, assuming the current net income of $20B and a price-to-earnings multiple of 100x (Bitcoin is a super high-growth company), you’d obtain a Bitcoin valuation of $2T. At a current price of roughly $1T, Bitcoin would be valued at 50x price-to-earnings which doesn’t seem too high given its rapid growth rate.

Don’t forget that Bitcoin’s net income grows faster than Tesla’s with its 100x P/E ratio!

Outlook

With nation states such as El Salvador adopting Bitcoin as a medium of exchange, millions of citizens are exposed to BTC not once every month but multiple times per day. Furthermore, millions of Bitcoiners are exposed to Bitcoin every single day—consuming Bitcoin content for hours each day.

And companies like Microstrategy and Tesla put Bitcoin into their treasury reserve assets.

“Orange-pilling” a single CEO or nation state leader results in an insanely high ROI that may be much higher than $10 for each $1 spent on advertisment. For example, if a blogger writes a blog post about Bitcoin he may reach only 1000 people, which we assumed is a marketing value equivalent of $50. However, a single CEO may decide to purchase $50,000,000 or even $50,000,000,000 worth of BTC as a result which is one billion times the ROI on this particular post.

For those types of extremely skewed distributions, the average (ROI on marketing spent) would be much higher than the median (ROI on marketing spent). If we’d forget the brand exposure that orange-pilled Michael Saylor, we’d significantly underestimate the average ROI on marketing spent and, consequently, our BTC valuation would turn out to be overly pessimistic. For instance, one billion impressions of the Bitcoin brand could easily result in $100 billion of capital flowing into the Bitcoin network in a given year, resulting in a massive $100 per single impression and $10,000 per 1000 impressions! Comparing this number to the $50 per 1000 impressions assumption of our above model shows that there’s a significant long-tail upward possiblity.

Considering these numbers, it becomes evident that Bitcoin may be hugely undervalued at the current point in time.

What’s the Value of a Single Bitcoin?

To answer this question, one would have to consider the growth of the annual cash flows of the “Bitcoin business” and perform a DCF analysis. I won’t do this here for clarity. Instead, let’s keep it simple and perform a short-term analysis using a simple P/E based valuation as a proxy. We start with a (pessimistic) current annual “net income” of $10B—what’s the value of a single Bitcoin for different P/E multiples?

| P/E Multiple | Bitcoin Total Value | BTC price |

|---|---|---|

| 10x | $100B | $4,761 |

| 20x | $200B | $9,523 |

| 50x | $500B | $23,809 |

| 100x | $1T | $47,619 |

| 200x | $2T | $95,238 |

I personally would set a multiple of 100x or even 200x due to the high network growth and the super conservative estimation of the “marketing value” above. So, BTC’s fair value today would be anywhere between $47k and $95k.

An interesting validation of this number is the current BTC price of roughly $40k — the market’s “wisdom of crowds” seems to agree with this valuation model.

Yet, I wouldn’t be surprised if the Bitcoin’s true “net income” would have to be set at $30B and a multiple of 200x is more appropriate given that Bitcoin belongs to the fastest-growing assets in the world. In that case, the fair market cap of BTC today would be $6T and the per-coin fair value would be $285k.